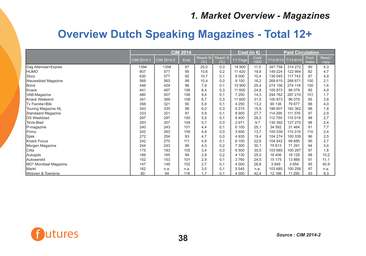

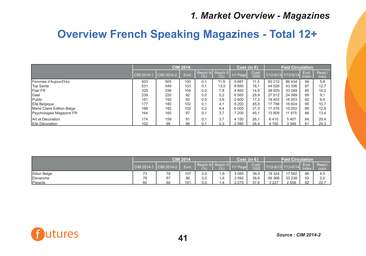

Overview Dutch Speaking Magazines - Total 12+

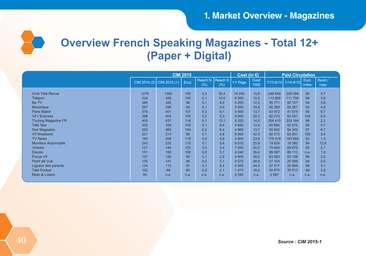

1. Market Overview Magazines

Dag Allemaal+Expres

HUMO

Story

Nieuwsblad Magazine

Bond

Knack

VAB-Magazine

Knack Weekend

Tv Familie+Blik

Touring Magazine NL

Standaard Magazine

DS Weekblad

TeVe-Blad

P-magazine

Primo

Sjiek

Knack Focus

Morgen Magazine

Citta

Autogids

Autowereld

MO* Mondiaal Magazine

Markt

Motoren & Toerisme

CIM 2014-1 CIM 2014-2

1394

607

630

569

446

441

480

341

356

343

333

297

283

240

242

272

242

244

175

166

152

147

162

80

1358

577

577

563

429

467

507

369

321

335

321

297

307

243

263

254

270

243

183

165

153

149

n.a.

94

CIM 2014

Evol.

97

95

92

99

96

106

106

108

90

98

97

100

109

101

109

93

111

99

105

99

101

102

n.a.

118

Cost ( in )

Reach N

(%)

25,0

10,6

10,7

10,4

7,9

8,4

9,4

6,7

5,9

6,0

5,9

5,5

5,7

4,4

4,9

4,7

4,9

4,3

3,4

2,9

2,9

2,7

3,0

1,7

Reach S

(%)

0,3

0,2

0,1

0,0

0,1

0,3

0,1

0,3

0,1

0,3

0,1

0,1

0,0

0,1

0,0

0,0

0,1

0,2

0,0

0,2

0,1

0,1

0,1

0,1

1/1 Page

14 900

11 420

6 000

9 100

10 900

11 600

7 250

11 600

4 250

5 315

8 900

8 400

2 971

6 100

3 600

4 935

6 100

7 300

6 500

4 130

3 760

4 000

5 545

4 000

Cost/

1000

11,0

19,8

10,4

16,2

25,4

24,8

14,3

31,5

13,2

15,9

27,7

28,3

9,7

25,1

13,7

19,4

22,6

30,1

35,5

25,0

24,5

26,8

n.a.

42,4

Paid Circulation

7/12-6/13 7/13-6/14

347 758 314 272

149 224 122 984

136 045 117 743

Evol.

Index

90

82

87

269 615 268 671 100

274 156 274 118

100 873 96 079

100

95

294 762 297 210 101

100 873 96 079

90 136

79 677

186 607 182 362

114 295 111 376

112 750 110 019

130 392 127 270

34 592

31 464

95

88

98

97

98

98

91

100 539 110 319 110

104 274 100 339

104 542 99 685

75 613

71 291

103 685 100 267

16 406

15 175

3 849

16 129

13 866

3 654

103 685 100 258

12 166

11 295

96

95

94

97

98

91

95

97

93

Read./

copy

4,3

4,7

4,9

2,1

1,6

4,9

1,7

3,8

4,0

1,8

2,9

2,7

2,4

7,7

2,4

2,5

2,7

3,4

1,8

10,2

11,1

40,9

n.a.

8,3

38

Source : CIM 2014-2

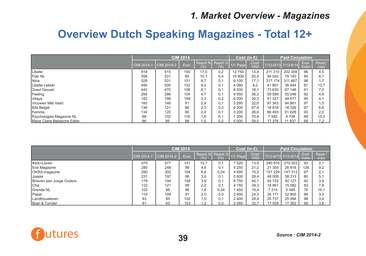

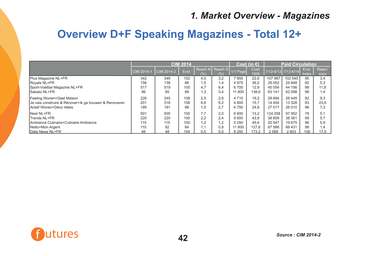

Overview Dutch Speaking Magazines - Total 12+

1. Market Overview Magazines

CIM 2014

Libelle

Flair NL

Nina

Libelle Lekker

Goed Gevoel

Feeling

Vitaya

Vrouwen Met Vaart

Elle België

Femma

Psychologies Magazine NL

Marie Claire Belgische Editie

CIM 2014-1 CIM 2014-2

919

558

528

490

442

256

182

160

136

134

88

86

915

531

531

500

470

266

198

146

121

120

102

85

Evol.

100

95

101

102

106

104

109

91

89

90

116

98

Reach N

(%)

17,0

10,1

9,7

9,0

8,1

4,7

3,3

2,9

2,3

2,4

1,6

1,5

Reach S

(%)

0,2

0,4

0,1

0,1

0,1

0,1

0,2

0,1

0,3

0,1

0,1

0,2

Cost ( in )

1/1 Page

12 750

10 900

9 100

4 080

8 500

9 650

6 000

3 295

8 200

3 200

7 200

5 000

13,9

20,5

17,1

8,2

18,1

36,2

30,3

22,6

67,8

26,6

70,6

59,0

Paid Circulation

Cost/

1000 7/12-6/13 7/13-6/14

Evol.

Index

211 310 202 008 96

94 042 79 140

84

317 174 311 467 98

41 891 36 494

73 630 67 148

59 589 55 048

51 327 48 617

97 343 94 861

18 918 18 326

66 493 61 628

7 582

6 708

17 376 11 837

87

91

92

95

97

97

93

88

68

Read./

copy

4,5

6,7

1,7

13,7

7,0

4,8

4,1

1,5

6,6

2,0

15,2

7,2

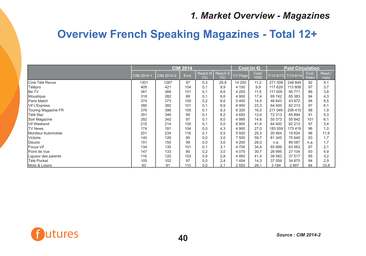

CIM 2014

Cost ( in )

Kerk+Leven

Eos Magazine

OKRA magazine

Joepie

Brieven aan Jonge Ouders

Ché

Grande NL

Pasar

Landbouwleven

Boer & Tuinder

CIM 2014-1 CIM 2014-2

570

280

290

231

179

122

102

119

83

61

577

248

302

197

194

121

88

109

85

63

Evol.

101

88

104

86

108

99

86

91

102

103

Reach N

(%)

10,7

4,6

5,6

3,6

3,6

2,2

1,6

2,0

1,5

1,2

Reach S

(%)

0,1

0,1

0,04

0,1

0,1

0,1

0,04

0,0

0,1

0,0

1/1 Page

7 520

5 250

4 690

5 600

8 750

4 750

1 450

2 650

2 400

2 060

13,0

21,2

15,5

28,4

45,1

39,3

16,4

24,3

28,4

32,7

Paid Circulation

Cost/

1000 7/12-6/13 7/13-6/14

Evol.

Index

290 916 270 053 93

21 355 26 918 126

151 229 147 313 97

48 008 38 313

54 725 50 127

18 861 15 582

7 214

5 485

34 171 32 905

25 737 25 094

17 559 17 262

80

92

83

76

96

98

98

Read./

copy

2,1

9,2

2,1

5,1

3,9

7,8

16,1

3,3

3,4

3,6

39

Source : CIM 2014-2